Styrene prices bottomed out in the third quarter of 2022 after a sharp decline, which was the result of a combination of macro, supply and demand and costs. In the fourth quarter, although there is some uncertainty about costs and supply and demand, but combined with the historical situation and relative certainty, styrene prices in the fourth quarter still have some support, or do not have to be too pessimistic.

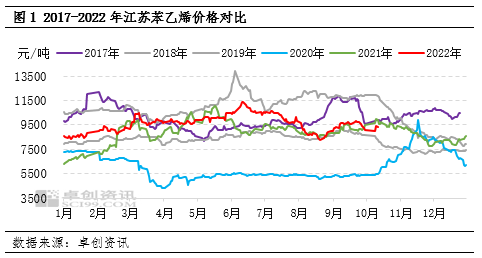

From June 10, styrene prices entered the downward channel, the highest price in Jiangsu on that day was 11,450 yuan / ton. on August 18, the low-end price of styrene in Jiangsu fell to 8,150 yuan / ton, down 3,300 yuan / ton, a drop of about 29%, making all the gains in the first half of the year back, but also down to the lowest price in the Jiangsu market in the past five years (except 2020). Then bottomed out and rose to the highest price of 9,900 yuan / ton on September 20, an increase of about 21%.

The combined effect of macro and supply and demand, styrene prices entered the downward channel

In mid-June, international oil prices began to turn, mainly due to the continued increase in U.S. commercial crude oil inventories. International oil prices fell sharply after the Federal Reserve announced the largest rate hike in nearly 30 years to fight inflation. It continued to influence the general trend in the oil market and the chemical market in the third quarter in anticipation of future rate hike cycles. Styrene prices fell 7.19% YoY in the third quarter.

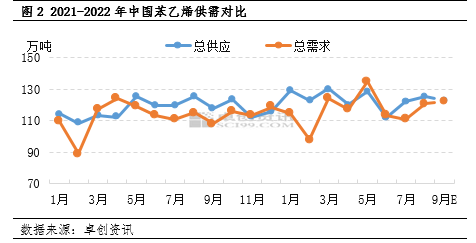

In addition to macro, supply and demand fundamentals had a significant impact on styrene prices in the third quarter. total styrene supply was much greater than total demand in July, and fundamentals improved in August when total demand growth was greater than total supply growth. in September, total supply and total demand were essentially flat, and fundamentals performed tightly. The reason for this change in fundamentals is that styrene maintenance units restarted one after another in the third quarter, and supply increased one after another; as downstream profits improved, new units came into operation, and the golden season was about to enter in August, end demand also improved, and styrene demand gradually increased.

The total supply of styrene in China in the third quarter was 3.5058 million tons, up 3.04% QoQ; imports are expected to be 194,100 tons, down 1.82% QoQ; in the third quarter, China’s downstream consumption of styrene was 3.3453 million tons, up 3.0% QoQ; exports are expected to be 102,800 tons, down 69% QoQ.

Chemwin is a chemical raw material trading company in China, located in Shanghai Pudong New Area, with a network of ports, terminals, airports and railroad transportation, and with chemical and hazardous chemical warehouses in Shanghai, Guangzhou, Jiangyin, Dalian and Ningbo Zhoushan, China, storing more than 50,000 tons of chemical raw materials all year round, with sufficient supply, welcome to purchase and inquire. chemwin email: service@skychemwin.com whatsapp: 19117288062 Tel: +86 4008620777 +86 19117288062

Post time: Oct-19-2022