Since August, the domestic price of acetic acid has been continuously rising, with an average market price of 2877 yuan/ton at the beginning of the month rising to 3745 yuan/ton, a month on month increase of 30.17%. The continuous weekly price increase has once again increased the profit of acetic acid. It is estimated that the average gross profit of acetic acid on August 21st was about 1070 yuan/ton. This breakthrough in the “thousand yuan profit” has also raised doubts in the market about the sustainability of high prices.

The traditional downstream off-season in July and August did not have a significant negative impact on the market. On the contrary, supply factors played a role in fueling the situation, transforming the originally cost dominated acetic acid market into a supply-demand dominated pattern.

The operating rate of acetic acid plants has decreased, benefiting the market

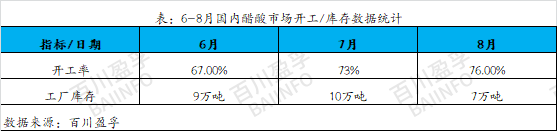

Since June, the internal equipment of acetic acid has been planned for maintenance, resulting in a decrease in the operating rate to a minimum of 67%. The production capacity of these maintenance equipment is relatively large, and the maintenance time is also long. The inventory of each enterprise continues to decline, and the overall inventory level is at a low level. Originally, it was thought that the maintenance equipment would gradually recover in July, but the recovery progress of mainstream equipment has not yet reached a fully operational state, with continuous alternations of start and stop, resulting in the restriction of long-term goods that could not be sold in quantity in June again in July, and market inventory continues to remain low.

With the arrival of August, the mainstream equipment for preliminary maintenance is gradually recovering. However, the scorching heat has caused frequent equipment failures from other manufacturers, and maintenance and fault situations have occurred in a concentrated manner. Due to these reasons, the operating rate of acetic acid has not yet reached a high level. After the accumulation of maintenance in the first two months, there was a shortage of goods in the market, leading to oversold situations among various enterprises in August. The market’s spot supply was extremely tight, and prices also climbed to their peak. From this situation, it can be seen that the shortage of spot supply in August was not caused by short-term speculation, but rather the result of long-term accumulation. From June to July, various enterprises effectively controlled the supply side through maintenance and troubleshooting, maintaining a relatively stable inventory of acetic acid. It can be said that this provided favorable conditions for the increase in acetic acid prices in August.

2. Downstream demand improves, helping the acetic acid market rise

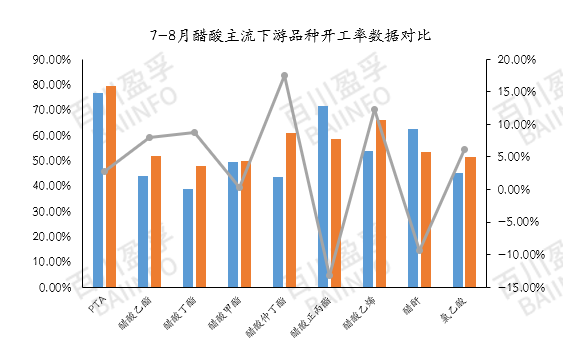

In August, the average operating rate of mainstream acetic acid downstream was about 58%, an increase of about 3.67% compared to July. This indicates a slight improvement in domestic downstream demand. Although the monthly average operating rate has not yet exceeded 60%, the resumption of production of certain products and equipment has had a certain positive impact on the regional market. For example, the average operating rate of vinyl acetate surged by 18.61% in August. The device restart this month was mainly concentrated in the northwest region, resulting in tight spot supply and a strong atmosphere of price increases in the region. Meanwhile, the operating rate of PTA is close to 80%. Although PTA has a small impact on the price of acetic acid, its operating rate directly reflects the amount of acetic acid used. As the main downstream market in East China, PTA’s operating rate has also had a positive impact on the acetic acid market.

Aftermarket analysis

Manufacturer maintenance: Currently, the inventory of various enterprises is maintained at a relatively low level, and the market is facing tight spot supply. Enterprises are very sensitive to inventory changes, and once inventory accumulates, there may be another situation of malfunction and production stoppage. Before inventory accumulates, the supply side remains relatively stable, and a slight “strategic adjustment” may have a positive boost effect on the market once again. It is expected that around August 25th, there will be maintenance plans for the main devices in Anhui region, which may overlap with the short-term maintenance time of the Nanjing device, while there are currently no regular maintenance plans announced in other regions. In this situation, it is even more necessary to closely monitor the fluctuations in inventory of each enterprise and the possibility of sudden device failures.

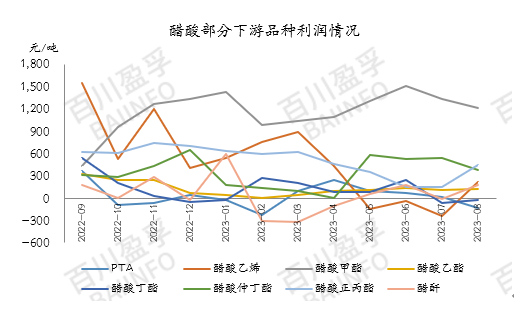

Downstream demand: Currently, upstream acetic acid inventory is still controllable, and downstream factories are temporarily maintaining production through short-term long-term contracts. However, the rapid rise in upstream acetic acid prices makes it difficult for downstream product pricing to fully transmit to end market demand. Some major downstream industries are facing profit pressure. Currently, among the main downstream products of acetic acid, except for methyl acetate and n-propyl ester, the profits of other products are almost on par with the cost line. The profits of vinyl acetate (produced by the calcium carbide method), PTA, and butyl acetate even show an inverted phenomenon. Therefore, a few enterprises have taken measures to reduce their burden or stop production.

Downstream industries are also watching to see if prices can be reflected in terminal profits. If the profits of downstream products decrease while the price of acetic acid remains high, it is expected that downstream production may continue to decrease to balance the profit situation.

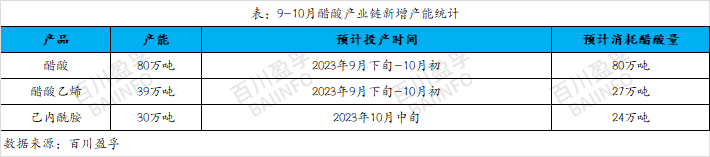

New production capacity: It is expected that by the end of September and early October, there will be a large number of new production units for vinyl acetate, totaling approximately 390000 tons of new production capacity, and it is expected to consume approximately 270000 tons of acetic acid. At the same time, it is expected that the new production capacity of caprolactam will reach 300000 tons, which will consume approximately 240000 tons of acetic acid. It is currently understood that the downstream equipment expected to be put into operation may start external production of acetic acid in mid September. Given the current tight spot supply in the acetic acid market, the production of these new equipment is bound to provide positive support for the acetic acid market once again.

In the short term, the price of acetic acid still maintains a high fluctuation trend, but the excessive increase in acetic acid prices last week caused increased resistance from downstream manufacturers, leading to a gradual reduction in burden and a decrease in purchasing enthusiasm. At present, there are some overvalued “foam” in the acetic acid market, so the price may fall slightly. Regarding the market situation in September, it is still necessary to closely monitor the production time of the new acetic acid production capacity. At present, the inventory of acetic acid is low and can be maintained until early September. If the new production capacity is not put into operation as scheduled before the end of September, downstream new production capacity may be procured for acetic acid in advance. Therefore, we remain optimistic about the market trend in September and need to keep an eye on the specific trends of the upstream and downstream markets, closely monitoring the real-time changes in the market.

Post time: Aug-22-2023